This is Part Three of my five-part, eight-week series on The Beginner’s Guide To Budgeting

Phew! Are you tired looking at all these numbers yet? Well, I hope not, but I do hope it’s at least making you REALLY aware of where your money is going. I bet you’ve never played with your money like this before?

Now that you’ve got the Big Picture of where all your money is going, it’s time to start budgeting, a.k.a. telling your money where to go. To me that is the essence of budgeting. Tell your money where to go or it’s going to tell you.

With all those categories you’ve broken down into more specific ones these are forever now considered your “budgets”. There’s a grocery budget, an out to eat budget, housing budget, etc. The amounts don’t always stay the same. As life goes, so goes our budgets. Family size grows, kids move away, our incomes rise and fall. You will have new life events that come and go that create a need for a new category/budget over time.

In Part Three we are going to focus on all of our categories except the Fun Life purchases Under False Finances (FLUFF), Misc., and other-wise unmentionable categories that you really don’t want to think about right now (i.e. little Fido’s monthly spa treatment). Let’s look at our basic Fixed Monthly Expenses (FME): Groceries, out to eat, toiletries, entertainment, personal grooming and the like. We’ll look at the other ones in Step Four.

CREATING ENVELOPES:

Take a look at all your categories you’ve written down (or put on a spreadsheet). Within each of these ‘budgets’ you now need to decide if they will come out of your checking account or if you will be paying for items by cash. I will tell you from experience it is a whole lot easier to keep track of your budgets if you pay for things with cash. Because trying to reserve $40 in checking for coffee every pay period (and doing the subtraction in your head after purchase) can get messy.

This is where envelopes come into play for our family. We have turned each of those categories or mini budgets into an envelope, except for our monthly bills (mortgage, utilities, student loan, etc. – those are paid by check or electronically) we use cash for everything else.

How you choose to manage these budgets is up to you. But the one item that we don’t pay cash for is gas. I don’t want to have to run into the store (leave my kids in the car) and pre-pay for my gas at the pump so we leave that “budgeted” amount in our checking and that is used for gas. We know that we spend approximately $40/week on gas so after each payday there is an extra $80 in checking to cover that.

1. Take out a box of envelopes (or buy one – it’s a good investment), tuck the flap inside and on the outside write the category.

One envelope for every category. See, nothing fancy. You can get cuter with your envelopes but for now let’s just focus on your money.

2. Write down the amount that will come out of each paycheck under the name.

This will be what you spent last month (or less!) and becomes your budgeted amount for that category for a time period (between paychecks).

Figuring out the envelope amounts:

All those categories you’ve been tallying and adding up become your monthly, weekly or bi-weekly budgets (depending on when you get paid). Those categories hold the dollar amount that you spent on that category for a period of time.

Say you have calculated that you spent $950 last month on groceries and you know that is way more than you should be spending because your spending was well over what you earned. You need to trim that down but you’re not sure by how much or what is even an average amount. It all depends on how much you need to feed your family. There are some guidelines of what you should spend out there but we have budgeted $150/week to feed our family of 5. Some weeks we go over. But in comparison to those guidelines that is well below the thrifty weekly plan for a family of 5.

You can start with that to give you a ballpark of where you should be in food spending. The beauty of this is it can always be adjusted next paycheck if necessary. Again this is always a work in progress. Budgeting is not a destination it’s a journey. But set an amount and see if you can stick to it for a pay period.

So back to our grocery envelope, if you determine that you will need $200/week for your family grocery budget and you get paid once every two weeks you would write down $400 on the envelope. Come next payday you will take out that amount of cash and put it in this envelope.

Take this envelope with you, or take a certain amount out, every time you grocery shop and when the money is gone, it’s gone. No borrowing from other envelopes. This really makes you think twice about impulse items and is a great motivator to create meal plans and figure out other ways to stretch your grocery budget.

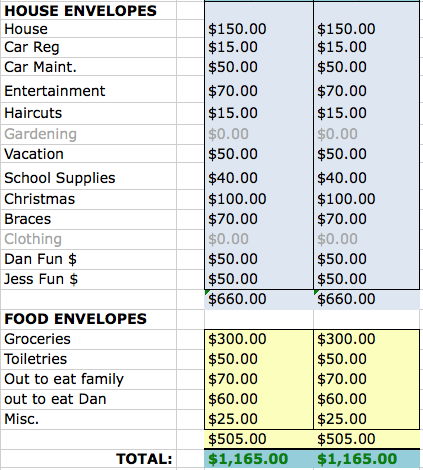

In the name of full transparency, here is our current envelopes:

You can see I have them split into Household and Food. These are our fixed monthly expenses (FME). This is off to the side of a spreadsheet I use to track all our fixed monthly bills (FMB) every month that come out of our checking so I know I have enough left to cover the total envelope amount. There is two columns because each one is a payday in the month of January.

The grayed out rows are ones that we aren’t allocating any cash to currently. This changes depending on the circumstances.

You will do this for every category that you spent money on during Part One, that will not be coming out of your checking for bills.

If any of those budgets are pushing you over your actual income then that is when you have to start getting creative. You will need to find ways in each budget to trim out the fat, or FLUFF items if they are in your basic FME categories. or move them to their own category to deal with in Part Four. Maybe brown bag your lunch 3 days a week or start doing your own nails.

Especially if your monthly income is LESS than the total amount of expenses you will need to decide what you want to cut from each category until those numbers match – your income is at least MORE than your total expenses. Or figure out ways to make more money.

3. Take the cash out of the bank on payday and put it into the designated envelopes

This is you telling your money where to go! You go, you.

(you can see these are well loved)

You will get to know your bank teller and will eventually get over the weirdness of taking large sums of money out every other week.

So do not spend any more money outside of your budgets and take those credit cards and freeze them in a block of ice if you have to, but DO NOT USE THEM

Come back next week for Part Four – The EX Factor. We’ll talk about those “fluffy” little life expected and unexpected things that seem to pop up constantly.